Exclusive: CATL Founder Upbeat About Ford Battery Plant Tie-Up, EVs Future in China

However, the battery giant faces problems, including EU regulatory issues and the difficulty of commercializing solid-state batteries, Zeng Yuqun tells Caixin

Rumored Pay Cap for State-Owned Securities Firms Fuels Debate

Speculation about a salary limit of $414,400 has top management fretting over the fate of their handsome remuneration

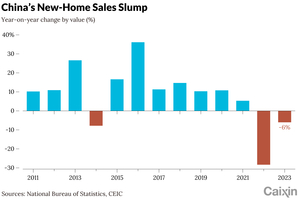

In Depth: Why China’s Project Whitelists Can’t Cure Real Estate Slump

Although the lists are helping many developers secure financing to finish their projects, there may not be enough demand for new homes to soak up the extra supply, bankers warn

Huawei’s Smartphone Comeback Tour Rolls On as New Pura 70 Models Sell Out

The Pura 70 Ultra and Pura 70 Pro sold out on Huawei’s online store on Thursday, the first day of their release, with photos on social media showing customers lining up at outlets in Shanghai

Exclusive: China Merchants Sends Bank Executive to Helm Mutual Fund Manager Bosera, Sources Say

Zhang Dong, CMB’s financial accounting head, is slated to become president of the asset manager

Gallery: World Press Picks Best Pics of 2023

The four global winners of the 67th World Press Photo Contest, which recognizes the best photojournalism and documentary photography from the past year, were selected from out of more than 61,000 entries. Conflicts often dominate the subjects of winning entries and this year was no exception, with the World Press Photo of the Year going to ‘A Palestinian Woman Embraces the Body of Her Niece,’ which was shot by Reuters photographer Mohammed Salem. Chinese photographer Wang Naigong won the Long-Term Projects, Asia category with her series of pictures titled ‘I Am Still With You,’ which documents the final years of a young mother dying of cancer

Apr 19, 2024 09:02 PM

China’s Top Court Highlights Juvenile Crimes Following Brutal Teenage Slaying

More than one-fifth of minor defendants involved in violent crime cases in the past three years were left-behind children, the court said, highlighting the importance of family supervision

Apr 19, 2024 08:21 PM

China’s High Court Weighs In on Sham Divorces

New judicial interpretation offers guidance on how lower court judges should apply the country’s Civil Code, including on cases involving property disputes between unmarried couples living together

Apr 19, 2024 07:48 PM

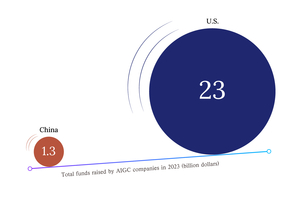

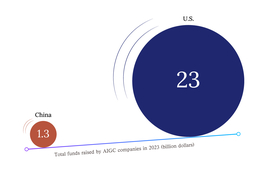

China Falls Far Behind U.S. in AI-Generated Content Funding, Investor Says

Chinese AIGC firms raised around $1.3 billion last year, compared with $23 billion by their U.S. counterparts

Apr 19, 2024 07:47 PM

Shanghai Composite Index Fell 0.29% on Friday

Shenzhen Component Index closed down 1.04%

Apr 19, 2024 03:03 PM

Daily Tech Roundup: TikTok Faces U.S. Reckoning, Huawei Unveils New Smartphone

Meituan names CEO of new core local commerce business, China looks to employ big data to tackle persistent misconduct in soccer

Apr 19, 2024 02:52 PM

Standard Chartered Dangles 10% Deposit Rate to Draw Mainland Cash

Lenders in Hong Kong are ramping up efforts to woo savers from the Chinese mainland and solidify the city’s status as a wealth hub

Apr 19, 2024 02:43 PM

Apple Pulls WhatsApp From China Store at Beijing’s Behest

The iPhone-maker, which has consistently complied with the country’s internet censorship regime, said regulators ordered the apps removed over national security concerns

Apr 19, 2024 02:08 PM

Hedge Funds Cry Foul Over Chinese Education Firm’s Default

An ad-hoc group of investors have accused XJ International of choosing not to pay its offshore debt even though its business is healthy and growing

Apr 19, 2024 01:55 PM

TSMC Cuts Chip Market Outlook as Consumer Weakness Persists

The world’s largest maker of advanced chips predicts growth of about 10% this year, scaled down from a previous forecast

Apr 19, 2024 01:42 PM

CX Daily: Why China’s Project Whitelists Can’t Cure Real Estate Slump

Intellectual property is a key issue for German companies dealing with China, Scholz says. IMF indicates it may raise China’s 2024 GDP forecast. Plus, the country looks to employ big data to tackle persistent misconduct in soccer.

Apr 19, 2024 10:06 AM

Shanghai Creates $18 Billion State Investment Giant

Merger of two investment firms will create a juggernaut providing financial backing to technology and innovation startups

Apr 19, 2024 04:44 AM

Hong Kong Spends $5.75 Million A Year on Idle Pandemic Makeshift Hospitals

Lawmakers urge government to press ahead with converting Covid isolation wards for non-medical use as maintenance costs mount

Apr 19, 2024 04:34 AM

TikTok Faces Washington Reckoning as Divest-or-Ban Vote Nears

TikTok legislation is to piggyback on a fast-moving aid package for Ukraine expected to be passed on Saturday

Apr 19, 2024 04:31 AM

China Restates Need for Steady Yuan Amid Fragile Confidence

PBOC says its goal is to maintain the basic stability of the yuan’s exchange rate and avoid excessive volatility

Apr 19, 2024 04:21 AM

Meituan Names Wang Puzhong as CEO of New Core Local Commerce Business

Food delivery giant looks to a younger generation for its management team as it refocuses on its core business

Apr 19, 2024 04:11 AM

Exclusive: ICBC Reshuffles Leadership at Core Department and Wealth Management Unit

Wang Hailu to be chair of ICBC Wealth Management, bringing experience in bond and foreign exchange trading

Apr 19, 2024 04:08 AM

- MOST POPULAR

- OPINION

- BLOG

- CAIXIN WEEKLY SNEAK PEEK

Al Translation BETA

- IN-DEPTH

- In Depth: How China’s Revision of Supervision Law Would Expand Legislative Oversight Powers

- In Depth: Fusion Sector Heats Up as China Pursues Next-Gen Nuclear Power

- In Depth: China’s Mammoth Effort to Help Foreigners Spend, Spend, Spend

- In Depth: Why China’s Middle Class Is Cutting Back on Private Daycare Centers

- In Depth: Frugality Bites for China’s Cash-Strapped Local Governments

Download Caixin App by

Scan & Download Caixin App

-

Available on App Store

Available on App Store

-

Get Android APP

Get Android APP

Follow Us

Copyright © 2024 Caixin Global Limited. All Rights Reserved.